TURN ABOUT IS FAIR PLAY

When it comes to resolving it's internal problems, nothing is ever simple at Priority One Credit Union in South Pasadena, California. During the month of June 2015, the credit union's attorney, John C. Steele of the Law Offices of Les Zieve in Irvine, California, filed a "Notice of Motion and Motion to Consolidate" ["the Notice"] seeking consolidation of the lawsuits filed by Priority One's insurance carrier, CUMIS, and the lawsuit filed by its former external auditor, Turner, Warren, Hwang, and Conrad.

The reasons for requesting consolidation is that the two lawsuits possess certain similarities including use of the same witnesses and documented evidence.

Under leadership of President Charles R. Wiggington, Sr., the number of lawsuits filed against and by the credit union have skyrocketed since his appointment on January 1, 2007. Lawsuits accusing Priority One of violating state and federal laws started in October 2010 when the former Branch Manager of the no longer existent Burbank office, accused the credit union of age and race discrimination. Over the three years that followed filing of that lawsuit, three other employees filed lawsuits alleging they were subject to sexual harassment, same-sex sexual harassment, retaliation, race discrimination, defamation of character and creation of a hostile working environment. The lawsuits were all voluntarily settled by the credit union with each Plaintiff signing an agreement that contained a disclaimer which declared that each settlement payment should not be construed as an admittance of wrong doing. In actuality, a settlement payments is an admittance that evidence possessed by a Plaintiff could result in an adverse judgment to the credit union. Furthermore, issuing a settlement payment avoids a potentially costly and embarrassing court trial and creation of a public record of the accusations, testimonies and final judgment.

Despite the payment of settlements, in 2013, President Wiggington and Vice President of Operations, Yvonne Boutte, boasted that the amount of each settlement were paltry and inconsequential to the credit union revealing once again, that Priority One's horrendous leadership have absolutely no concept of the detrimental impact lawsuits have upon a business.

In 2013, an officer of the Credit Union and more than likely, a member of the Credit Resolutions Department, posted comments about a Member and her then delinquent loan, throughout the Internet. The Member sued the Credit Union and within fix months, her complaint was voluntarily settled by Priority One. The settlement included:

- Writing off her remaining unpaid loan balance

- Removal of all adverse references from her credit union

- Issuance of a letter signed by President Wiggington admitting that someone disparaged the Member but denying he authorized the violation of the Privacy Act; and

- Paying the Member a settlement in the amount of almost $20,000 to avoid a costly and potentially embarrassing court trial.

To provide some understanding of the complexities involved in each of the current lawsuits, we are now providing summaries of all pre-trial meetings so far conducted. Remember, none of the lawsuits have actually proceeded to trial. It is also important to note that on June 4, 2015, Priority One's attorney filed a counter-complaint against the credit union's former external auditor, Turner, Warren, Hwang and Conrad.

CUMIS VS TWHC

Case Number BC541935

06/09/2015 Proof of Service

Filed by Attorney for Defendant/Respondent

06/09/2015 Order (GRANTING MOTION TO ADMIT ATTORNEY PRO HAC VICE )

Filed by Court

05/15/2015 Declaration of Diligence (Deposition Subpoena Served on Cynthia Villamin )

Filed by Attorney for Pltf/Petnr

05/15/2015 Motion in Limine (for an Order Excluding Any Expert Report by Defendants' Witness Michael J. Sacher, CPA; P's & A's; Declaration of Patrick J. Collins in Support thereof; [Proposed] Order thereon)

Filed by Attorney for Plaintiff/Petitioner

05/12/2015 Notice of Ruling

Filed by Attorney for Defendant/Respondent

05/04/2015 Statement-Case Management

Filed by Attorney for Plaintiff/Petitioner

05/01/2015 Receipt ( jury fees $150 )

Filed by Attorney for Defendant/Respondent

05/01/2015 Statement-Case Management

Filed by Attorney for Defendant/Respondent

04/29/2015 Statement-Case Management

Filed by Attorney for Defendant/Respondent

04/17/2015 Declaration of Diligence

Filed by Attorney for Plaintiff/Petitioner

04/14/2015 Notice of Change of Address

Filed by Attorney for Plaintiff/Petitioner

04/14/2015 Notice (OF STATUS CONFERENCE RE: RELATED CASES AND CONT CMC )

Filed by Attorney for Plaintiff/Petitioner

04/08/2015 Motion (TO ADMIT ATTORNEY PRO HAC VICE )

Filed by Attorney for Plaintiff/Petitioner

03/13/2015 Notice of Ruling

Filed by Attorney for Plaintiff/Petitioner

01/16/2015 Order (RE EX PARTE OF 01/16/15 )

Filed by Court

01/16/2015 Ex-Parte Application (DEFENDANT'S EX PARTE )

Filed by Attorney for Defendant/Respondent

01/08/2015 Notice-Related Cases

Filed by Attorney for Plaintiff/Petitioner

10/01/2014 Stipulation and Order

Filed by Court

08/18/2014 Notice of Association of Attorneys

Filed by Attorney for Plaintiff/Petitioner

08/18/2014 Notice of Ruling

Filed by Attorney for Plaintiff/Petitioner

07/18/2014 Notice of Motion (TO ADMIT ATTORNEYS PRO HAC VICE )

Filed by Attorney for Plaintiff/Petitioner

06/13/2014 Cross-complaint

Filed by Attorney for Cross-Complainant

06/13/2014 Summons Filed

Filed by Attorney for Cross-Complainant

05/30/2014 Statement-Case Management

Filed by Attorney for Defendant/Respondent

05/30/2014 Statement-Case Management

Filed by Attorney for Plaintiff/Petitioner

05/20/2014 Proof of Service

Filed by Attorney for Plaintiff/Petitioner

05/16/2014 Answer

Filed by Attorney for Defendant/Respondent

05/02/2014 Proof of Service

Filed by Attorney for Plaintiff/Petitioner

04/23/2014 Notice-Case Management Conference

Filed by Clerk

04/07/2014 Complaint

Filed by Attorney for Plaintiff/Petitioner

TWHC VS PRIORITY ONE CREDIT UNION

Case Number EC063303

07/01/2015 at 10:00 am in department 71 at 111 North Hill Street, Los Angeles, CA 90012

Motion for Leave

08/18/2015 at 10:00 am in department 71 at 111 North Hill Street, Los Angeles, CA 90012

Status Conference(& R/C BC541935)

08/24/2015 at 10:00 am in department 71 at 111 North Hill Street, Los Angeles, CA 90012

Status Conference(& R/C BC541935)

Documents Filed (Filing dates listed in descending order)

06/04/2015 Motion for Leave

Filed by Attorney for Defendant/Respondent

06/04/2015 Motion

Filed by Attorney for Defendant/Respondent

05/06/2015 at 10:00 am in Department 71, Suzanne G. Bruguera, Presiding

Status Conference (RE RELATED CASE AND CONT'D CMCFROM 04/06/15) - Completed

05/11/2015 at 10:30 am in Department 71, Suzanne G. Bruguera, Presiding

Telephonic Conference (& REL'D BC541935) - Completed

04/14/2015 Notice of Status Conference filed (RE RELATED CASES AND CONT CMC )

Filed by Attorney for Defendant/Respondent

04/06/2015 at 09:30 am in Department 71, Suzanne G. Bruguera, Presiding

Conference-Case Management - No Appearance

03/06/2015 at 03:30 pm in Department 71, Suzanne G. Bruguera, Presiding

Nunc Pro Tunc Order - Completed

03/16/2015 Notice of Ruling

Filed by Attorney for Defendant/Respondent

02/27/2015 Notice-Case Management Conference

Filed by Clerk

02/02/2015 Answer (TO COMPLAINT )

Filed by Attorney for Defendant

01/09/2015 Proof of Service (OF SUMMONS, COMPLAINT, CIVIL CASE COVER SHEET, CIVIL CASE COVER SHEET ADDENDUM AND STATEMENT OF LOCATION, NOTICE OF ORDER TO SHOW CAUSE RE FAILURE TO COMPLY WITH TRIAL COURT DELAY REDUCTION ACT...)

Filed by Attorney for Plaintiff

12/24/2014 Notice (OF RELATED CASE (BC541935 )

Filed by Attorney for Plaintiff

12/24/2014 Proof of Svc of Summons & Co./Ptn.

Filed by Attorney for Plaintiff

12/05/2014 Notice-Case Management Conference

Filed by Clerk

12/05/2014 OSC-Failure to File Proof of Serv

Filed by Clerk

12/05/2014 Complaint filed-Summons Issued

12/05/2014 Summons Filed

The lawsuits filed by (1) CUMIS against Turner, Warren, Hwang and (2) the lawsuit filed by Turner, Warren, Hwang and Conrad against Priority One Credit Union and (3) now, the lawsuit (cross-complaint) filed by Priority One Credit Union against Turner, Warren, Hwang and Conrad have absolutely nothing to do with proving who physically walked out of the Los Angeles branch during the years of 2010-2012 with $1 million in cash in their possession. This prompts us to wonder what has happened to CUMIS' initial complaint file against accused embezzler, Pearl Lynnette Fortson?

Historically, Ms. Fortson like every executive of Priority One Credit Union, was a mediocre Branch Manager and later, an even more mediocre AVP. However, her limitations aside, she apparently was a mastermind of no small stature when she inconspicuously and almost invisibly, walked out of the Los Angeles branch with more than $1 million in cash.The fact that she did so without detection by any of the Credit Union's overpaid officers, the evidently comatose Supervisory Committee and the brain dead Board of Directors is amazing.

CUMIS is exerting tremendous effort to build a case around Turner, Warren, Hwang and Conrad's alleged violation of established auditing standards which resulted in subpar reports provided to the Supervisory Committee who afterwards, compiled erroneous assessments of Priority One's actual financial performance and its internal security protocols. This is at least, what CUMIS hopes a jury will believe.

Certainly CUMIS is desperate to recuperate the monies paid to Priority One against the Credit Union's $1 million claim yet doesn't it seem at all peculiar that CUMIS is placing blame on Turner, Warren, Hwang and Conrad who had absolutely nothing to do with the physical removal of more than $1 million in cash from the Los Angeles branch.

Here is status of Ms. Fortson's case:

: CUMIS is exerting tremendous effort to build a case around Turner, Warren, Hwang and Conrad's alleged violation of established auditing standards which resulted in subpar reports provided to the Supervisory Committee who afterwards, compiled erroneous assessments of Priority One's actual financial performance and its internal security protocols. This is at least, what CUMIS hopes a jury will believe.

Certainly CUMIS is desperate to recuperate the monies paid to Priority One against the Credit Union's $1 million claim yet doesn't it seem at all peculiar that CUMIS is placing blame on Turner, Warren, Hwang and Conrad who had absolutely nothing to do with the physical removal of more than $1 million in cash from the Los Angeles branch.

Here is status of Ms. Fortson's case:

CUMIS VS PEARL LYNNETTE FORTSON

Case Number BC542611

- In a declaration filed on December 11, 2014, CUMIS' attorney, David R. Bence, states that during an August 1, 2014 hearing, he informed the court that Ms. Fortson had filed for bankruptcy protection. At the time, the court scheduled a bankruptcy status meeting for October 30, 2014.

- On October 3, 2014, Mr. Bence appeared in court and disclosed that his client, CUMIS, was preparing to file an Adversary Complaint. At the time, the Court set a bankruptcy conference for July 30, 2015, however, Mr. Bence later claimed that he never received a notice from the court advising him that the conference had been rescheduled to December 8, 2014.

- A status conference has now been scheduled to take place on August 5, 2015 at Superior Court in Los Angeles.

Ms. Fortson's filing for bankruptcy protection is actually quite clever. If approved, she will not have to pay restitution for the money she allegedly embezzled.

During the years of 2010 through 2013 Priority One's annual spending on legal skyrocketed from approximately $20,000 to $22,000 spent in the years while William E. Harris served as President and CEO, to an unprecedented more than $120,000 (per year).

Frustrated with our periodic publication of the Credit Union's legal expenditures, in 2014, President Wiggington ordered removal of the credit union's monthly and annual legal expenses from its Income Statement/Balance Sheet. President Wiggington's efforts to hide the amount spent on "legal" is hardly necessary to gauge its effect upon the Credit Union's financial performance. Since 2008, President Wiggington has exacted tremendous effort to ensure Net Capital remains well above 6%. This meant closing branches, implementing a company-wide wage freeze that affected everyone but the executive sector. He also reduced spending on marketing, advertising and business development and ceased almost all together, the credit union's involvement in community and chamber sponsored events. The end result has been a continual struggle to try and garner new business and members. The credit union's efforts have been continually been undermined by growing disinterest by Members and potential Members in the financial products offered by the credit union coupled by a large number of account closures. The failure to generate consistent high profits have also impacted the Credit Union's ability to pay its bills. As Bankrate.com has reported each year since 2011, Priority One's suffers from "above normal overhead."

It is clear that Priority One's high legal expenses which increased to a total of more than $500,000 during the years of 2010-2013, are heavily taxing the credit union. The added expenditures pay for attorneys who work frantically to fabricate defenses that are intended to help Priority One escape retribution for the failures, abuses and negligible behaviors committed by the President, the Board of Directors, and the Supervisory Committee.

But First......

Due to the over 40-pages of legal documents filed by the Credit Union on June 4, 2015, we will have to continue our reporting about the lawsuits over the next 1 or two publications. However, at this time we'd like to report on other events occurring at Priority One that are not related to the lawsuits.

RAISES FOR SOME EMPLOYEES

The Credit Union announced during its April 2015 all staff meeting that following a more than four (4) year wage freeze, there would be a PARTIAL lifting of the company's four-year wage freeze.

To be accurate, the four-year freeze never affected every single employee of the credit union. The wage freeze was officially introduced in late 2010 by President Wiggington and then COO, Beatrice Walker. The reason why the freeze was implemented is that Priority One was not obtaining the level of new business needed to offset its expenditures. At the time, net capital had dropped to 6.8% and the DFI informed the President that he needed to raise net capital, suggesting he streamline operations including, close branches that were not operating at optimum.

Despite implementation of the freeze, at the end of 2010, the President received a bonus from the Board of Directors and in the years since 2010, has received annual bonuses and raises. His failures, illegal acts and immersion in scandals were evidently inconsequential to the Board of Directors and the loss of more than $20 million in net income and the filing of numerous lawsuits were of absolutely no consequence to his continue stay as Priority One's worst President and CEO in its more than 87 year history.

The partial lifting of the freeze should not be construed as an indicator that business has improved. The credit union remains in a financial slump and as we saw in 2014 and 2015, he continues to hide the organization's annual reports.

In 2010, we witnessed a similar incident. In February 2010, President Wiggington and then COO, Beatrice Walker, spread rumors that Priority One had generated profits during the month of January. As evidence to profit, the Income Statement/Balance Sheet for the month of January 2010 showed profits in excess of $100,000. The claims to profit seemed suspicious because the credit union ended 2009 more than $5 million in the negative. By March 2010, a representative of the Accounting Department revealed that the President and Ms. Walker transferred monies from one of the credit union's general ledgers and reported the "borrowed" money as profits where no profit had occurred. The year ended with income more than $500,000 in the negative.

FINALLY, THE DEPARTURE OF JOSEPH GARCIA

Joseph Garcia, the man who was once known as former COO, Bea Walker's number one confidant and who over a two-year period was promoted from Call Center Supervisor to Consumer and Real Estate Loan Department Manager, Credit Manager and later demoted to Consumer Loan Manager and demoted again to Assistant Consumer Loan Manager and promoted to AVP of Sales and Business Development and finally, demoted to Business Development Representative and who failed at every position he held, has finally department the credit union on his own volition. He won't be missed.

In 2010, Mr. Garcia provided false testimonies to the President which facilitated the expulsion of several employees the President, then COO, Beatrice Walker, and Executive Vice President, Rodger Smock, labeled enemies of their regime.

By early 2011, Mr. Garcia's relationship with his former benefactor, Beatrice Walker, had deteriorated and having discovered that she had targeted him for termination, the cowardly Mr. Garcia fled the credit union on a medical leave alleging he was suffering from stress.

While on medical leave, Ms. Walker was terminated and Mr. Garcia returned to work shortly thereafter.

He spent the next two months, wooing the President and by November 2011, the obtuse Mr. Wiggington promoted Mr. Garcia to Vice President of Sales and Business Development. Mr. Garcia promised he would "force" employees to perform or they would suffer termination. With then Chief Loan Officer, Cindy Garvin, the two developed quotas for every employee and on February 2, 2012, launched their new program. Over the next eight months, Mr. Garcia and Ms. Garvin orchestrated the termination of many new and long-time employees for failing to attain their quotas. By October 2012, it was obvious that Mr. Garcia's strategies had all failed. Frustrated, Ms. Garvin threatened to terminate him and he again, fled the credit union on yet another medical leave of absence again alleging work induced stress. In December 2012, Ms. Garvin was terminated and Mr. Garcia returned to work in January though upon his return, he was advised that he was being demoted to the post of Priority One's one and only Business Development Representative. At the time, he was assigned a monthly quota of $150,000.

Over the next two years Mr. Garcia never attained his quota. His highest number of loans funded for a single month approximated $30,000. Despite his gross failures, the President exempted him from the credit union's policy which explicitly stated employees who failed to attain their quotas during a consecutive two-month period would be terminated.

Over the next two years, Mr. Garcia became another useless fixture of the credit union, contributing absolutely nothing to the betterment of the company.

In the weeks preceding his May departure, Mr. Garcia was sent to work at the Van Nuys branch in the position of interim Branch manager. While there, he complained that his employer was forcing him to drive each day from his residence in Montclair to Van Nuys and that he had grown weary of being taken advantage of.

Before being unceremoniously terminated in July 2011, then COO, Beatrice Walker, used to boast that if you wanted to force an employee to resign, all you had to do was transfer the, to a branch that was located furthest from their home. Mr. Garcia, the man who was a polarizing presence in the credit union and who was responsible for the termination of dozens of employees in 2012, and who failed in every capacity he served in, fell victim to Bea Walker's infamous ploy, finally driven out by President Wiggington.

A NEW CFO? NOT EXACTLY

What do you get when you can no longer afford to hire a CFO? You hire a Controller. Of course a CFO is not synonymous with being a Controller though President Wiggington is hoping to force a change in what defines the responsibilities of a Controller.

In 2014, the President revealed that he and Board Chair, Diedra Harris-Brooks, and Executive Vice President, Rodger Smock, agreed that when a new CFO was hired to replace former CFO, Saeid Raad, that no announcement would be posted by the credit union. Their reasoning was that they didn't want the information to find its way to the Internet.

In 2014, the credit union hired a Controller to fill the position vacated by Saeid Raad. However, the position to hire a Controller versus a CFO, was economics. The fact is, Priority One could no longer afford to pay a salary of $140,000 or more, to a new CFO. So they opted for a more economical alternative. The Controller is Simona Hollins who prior to her arrival at Priority One, worked for SH Account Services and obtained an MBA in Accounting from the University of Phoenix.

This is not the first time Priority One has had a Controller. After the departure of CFO, Manny Gaitmaitan, at the end of 2009, the President convinced the Board of Directors that he could promote then Accounting Supervisor, Jennifer Kelly, to the post of Controller and that she would be able to perform most of the responsibilities once performed by Mr. Gaitmaitan. Ms. Kelly proved that a Controller is not a CFO and her stint as Controller was short-lived.

Additionally, Turner, Warren, Hwang and Conrad states that the theft of more than $1 million was the result of acts committed by unnamed "others" and not their firm. So who are these "others" who allegedly committed acts including dispensing advice which created the opportunity for the theft of more than $1 million?

Unlike her predecessor, Mr. Raad, who was introduced to the Credit Union through his then friend, COO, Beatrice Walker, Ms. Hollins does not appear to have a business association with either the President or members of his executive sector.

Unlike Mr. Raad who was introduced to the credit union by his former friend and associate, Beatrice Walker, Ms. Hollins does not appear to have been hired as a result of cronyism. Hopefully, she won't compromise ethics and like Mr. Raad, choose to manipulate the credit union's financial reporting practices.

THE WILD WEST

Due to the amount of documentation filed by CUMIS, Turner, Warren, Hwang and Conrad and more recently, by Priority One Credit Union's attorney, we will only provide a small portion of the documents proving the reasons why the various Plaintiffs have filed complaints against one another.

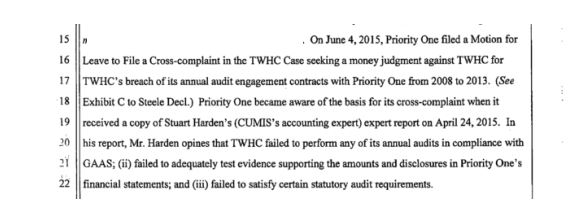

On June 4,2015, John C. Steele, attorney for the credit union filed the notice seeking consolidation accompanied by a counter-complaint filed by his client and alleging breaches of contract by Turner, Warren, Hwang and Conrad during each year (2008-2013) when the outside auditor provided reports based on audits that were conducted out-of-compliance to established and mandated auditing standards. Mr. Steels begins by presenting the facts underlying the lawsuits brought be each party.

Memorandum Points and Authorities

II. Statement of Facts

II. Statement of facts.

Priority One entered into a business relationship with Turner, Warren, Hwang and Conrad on March 31, 2008 and which continued until March 31, 2013. In February 2013, an audit of the Los Angeles branch's records revealed that more than $1 million in cash had been embezzled by Pearl Lynnette Fortson who CUMIS identifies as the Branch Manager of that office. The thefts occurred over a two-year period, 2010-2012, and began either in "early" or "late" 2010 and continued through 2012. In their lawsuit, CUMIS makes the following statements:

- Ms. Fortson embezzled the money by herself or with accomplices.

- The thefts began either in “early” or “late” 2010 and continued through 2012.

- In February 2013, on the date she was terminated, Ms. Fortson served in the capacity of Branch Manager of the Los Angeles office.

- Did Ms. Fortson steal more than $1 million in cash during the years of 2010 through 2012 by herself and without assistance or was she aided by an accomplice(s)?

- Why couldn't CUMIS' experts obtain a more precise date when the thefts occur. Did these begin in "early" 2010 or "late" 2010?

- CUMIS identifies Ms. Fortson as the Branch Manager of the Los Angeles branch on the date she was terminated but Ms. Fortson was actually an AVP and had not been a Branch Manager since 2007.

Discrepancies with information seem to be a chronic problem with anything related to Priority One. At times, the discrepancies are intentional, such as when President Wiggington chooses to manipulate reporting. In regards to the Notice filed on April 4, 2015, CUMIS states it reviewed the evidence provided by Priority One Credit Union regarding the theft of more than $1 million from the Los Angeles branch's vault. CUMIS' review concluded that Priority One's "employee dishonesty claim" possessed sufficient merit justifying payment of the claim. CUMIS paid the $1,005,376.00 claim minus the $25,000 deductible for a total of $980,055.10.

Following payment of the claim, CUMIS next entered into a settlement agreement with Priority One which allowed CUMIS to seek recovery of the monies paid against the credit union's claim. Legal ease aside, this should not be construed to mean that CUMIS filed a lawsuit on behalf of the credit union but that they are trying to recuperate every penny paid against the claim in addition to any other awards the court may deem appropriate.

Based on the information contained in the Notice, its now clear that on April 24, 2014, the date CUMIS filed its lawsuit against Turner, Warren, Hwang and Conrad, they had not gathered the evidence needed to prove their allegations against the external auditor. The inaccuracies and uncertainties we've described suggest that CUMIS filed their lawsuit to ensure filing occurred within the statute of limitations allotted under law. By doing so, CUMIS could amend their complaint at a later date. What's more, the Notice which was filed on June 4, 2015, slightly more than one year after CUMIS filed its lawsuit, reveals that one of CUMIS' "experts" founded enough additional evidence of wrong doing allegedly perpetrated by Turner, Warren, Hwang and Conrad allowing Priority One to file a counter-complaint against their former external auditor.

Though there is nothing illegal about CUMIS' actions, the Notice suggests that the insurance carrier is quite desperate to recuperate the monies paid against Priority One's claim. Their desperation is sufficient that they were able, after one year, to provide Priority One Credit Union information that allowed the credit union to file a counter-complaint. If we didn't know better, we might think that CUMIS is trying to bombard Turner, Warren, Hwang and Conrad with as many complaints and allegations of wrong doing to sway a jury to issue a judgment in their favor.

CUMIS' CASE

Specifically, CUMIS accuses Turner, Warren, Hwang and Conrad of:

- Failing to perform annual financial statement audits of the credit union "in compliance with professional standards governing:

- CPA auditors

- Federal regulations governing audits of credit unions

- Violating the terms of its agreements with Priority One for each year from 2008 through 2013

TURNER, WARREN, HWANG

AND CONRAD'S CASE

Priority One's attorney, John C. Steele, takes a moment to over emphasize that on "December 5, 2014- eight months after CUMIS filed its Complaint- TWHC filed a lawsuit in Los Angeles Superior Court (Case No. ECO63303), seeking a money judgment against Priority One for Priority One's failure to pay $68,299.79 in alleged monies owned to TWHC for the post-embezzlement investigation and preparation of a report." Mr. Steele's caddy tone is not lost on us.

He continues, stating that Turner, Warren, Hwang and Conrad seeks payment of $68,299.79 which the credit union failed to pay for services rendered. Doesn't it serve as a poor example when a credit union- a financial entity, that claims to be a "financial fitness center", refuses to pay its debts?

- According to Mr. Steele, Turner, Warren, Hwang and Conrad's lawsuit accuses Priority One of breaching the agreement entered into with Turner, Warren, Hwang and Conrad.

- Furthermore, Turner, Warren, Hwang and Conrad seek quantum meruit which simply means they seek "a reasonable sum of money" to pay for services rendered and work completed at the request of the Credit Union.

- Lastly, Turner, Warren, Hwang and Conrad ask the court for any amount due on open book account.

Priority One

Credit Union's Cross-Complaint

The disclosures made by Priority One's attorney, seems to indicates that since the thefts were discovered in February 2013, the credit union has remained in a stupor completely oblivious to the alleged failures committed by Turner, Warren, Hwang and Conrad and only realized in April 2015 that the reports provided to them in 2008, 2009, 2010, 2011, 2012 and 2013 were immersed in deficiencies. Clearly Priority One remains lost in a fog and like their inability to protect credit union and Member assets, it seems that they are quite oblivious to the validity of the records they utilize in forecasting the Credit Union's future performance or in assessing the effectiveness of its security protocols.

FACTS

CUMIS has accused Turner, Warren, Hwang, and Conrad of negligible auditing practices.

CUMIS alleges that if it weren't for these negligible practices, Turner, Warren, Hwang and Conrad would have noticed the thefts allegedly perpetrated by former AVP, Lynnette Fortson, which would have brought and end to the thefts.

Though the subject of auditing standards is important to ensure reports provided to the Credit Union are accurate for the purpose of developing projections and assessments, the FACT remains, Turner, Warren, Hwang and Conrad had absolutely no involvement in the physical removal of cash from the Los Angeles branch.

According to the cross-complaint filed earlier this month by Priority One Credit Union, shoddily compiled reports produced by Turner, Warren, Hwang and Conrad were provided to the Credit Unions for the years 2008 through 2013. As a result, the Supervisory Committee created erroneous assessments based on the information provided by the external auditor.

2009: An audit performed by Turner, Warren, Hwang and Conrad revealed that more than $60,000 were stolen by a former receptionist of the Los Angeles branch.

CUMIS alleges that if it weren't for these negligible practices, Turner, Warren, Hwang and Conrad would have noticed the thefts allegedly perpetrated by former AVP, Lynnette Fortson, which would have brought and end to the thefts.

- So why didn't Priority One's internal security protocols ever identify a single theft allegedly perpetrated by the former AVP?

- Why didn't the Accounting Department which oversees cash sent to and received from all branches never identify a single discrepancy?

- Why didn't the Credit Union's Vice President of Compliance ensure that all branches were carrying out banking procedures pursuant to state and federal mandates and credit union policy?

- Why didn't the Supervisory Committee perform its due diligence and personally conduct its own audits of branch cash? Is it customary for the Supervisory Committee to rely solely on the reports provided by external auditors or do they take the initiative to verify the accuracy of the information they're provided?

- How did the AVP transport more than $1 million in cash from the Los Angeles vault without ever being observed by branch personnel?

- What exactly does President Wiggington do to ensure security protocols are being performed by branch staffs?

- How does Priority One's Vice President of Operations ensure that security measures are maintained and when necessary, amended?

2009: An audit performed by Turner, Warren, Hwang and Conrad revealed that more than $60,000 were stolen by a former receptionist of the Los Angeles branch.

2010: A married couple, knowingly withdrew more than $100,000 from their HELOC checking account even though the term of the HELOC had expired. When asked to repay the monies, the couple refused. CUMIS' investigator interviewed current and former employees of the Real Estate Loan Department who all confirmed the Credit Union was at times negligent about closing HELOCs. Despite the admittance of negligence, CUMIS paid the claim.

With regards to the latest claim filed by the Credit Union, CUMIS paid $980,055.10 against the Credit Union's claim of $1,005,376.00. CUMIS' decision to pay the credit union's claims is enigmatic since the question of the effectiveness of Priority One's security protocols should be scrutinized and further investigated.

The credit union's refusal to pay the money owed Turner, Warren, Hwang and Conrad for services rendered following discovery in February 2013, that former AVP, Pearl Lynnette Fortson, embezzled more than $1 million, would not be the first time the organization drags its perennial feet to pay it debts. In 2010, then CFO, Saeid Raad, instructed the Accounting Department to withhold issuing payment on all invoices for at least 4 weeks after they were received by the Credit Union. He also ordered that employee reimbursements be paid out once per month which created a financial hardship to many of the Credit Union's low paid staff. His reason for withholding payments was because Priority One Credit Union did not have sufficient money budgeted to pay its expenses. Despite strained finances, President Wiggington would continue to insist over the next four years that business was great and the Credit Union., experiencing a financial resurgence. His statements were utterly untrue.

With regards to the latest claim filed by the Credit Union, CUMIS paid $980,055.10 against the Credit Union's claim of $1,005,376.00. CUMIS' decision to pay the credit union's claims is enigmatic since the question of the effectiveness of Priority One's security protocols should be scrutinized and further investigated.

The credit union's refusal to pay the money owed Turner, Warren, Hwang and Conrad for services rendered following discovery in February 2013, that former AVP, Pearl Lynnette Fortson, embezzled more than $1 million, would not be the first time the organization drags its perennial feet to pay it debts. In 2010, then CFO, Saeid Raad, instructed the Accounting Department to withhold issuing payment on all invoices for at least 4 weeks after they were received by the Credit Union. He also ordered that employee reimbursements be paid out once per month which created a financial hardship to many of the Credit Union's low paid staff. His reason for withholding payments was because Priority One Credit Union did not have sufficient money budgeted to pay its expenses. Despite strained finances, President Wiggington would continue to insist over the next four years that business was great and the Credit Union., experiencing a financial resurgence. His statements were utterly untrue.

And though Priority One is using the allegations against Turner, Warren, Hwang and Conrad to refuse issuing payment to its former external auditor, we believe that the refusal to pay is related to the Credit Union's strained finances and its continually looming overhead which does not abate because of Priority One's floundering business development efforts.

There was a time, when the Supervisory Committee used to frequently visit each of Priority One's branch's and physically counted money in the vaults for the express purpose of ensuring cash balanced with the amounts of cash recorded in vault ledgers. Since Charles R. Wiggington, Sr. was appointed President and since both Cornelia Simmons became the committee's Chairperson, the practice that ensured safety, has been discarded.

What's more, under Ms. Simmons, the committee does not meet on a monthly basis as it did when William E. Harris Was President. We believe the committee's minutes should be subpoenaed to prove how often they meet, what topics are discussed during their meetings, and which of the credit union's security measures have been reviewed and which which have been updated and amended.

Though we intend to continue our dissection of the more than 40 page Notice submitted by Priority One's attorney in our next publication, we'd like to briefly describe Turner, Warren, Hwang and Conrad's responses to each of the accusations leveled by CUMIS in their complaint filed with the Superior Court of California. Turner, Warren, Hwang, and Conrad provided a total of twenty-six Affirmative Defenses in their reply. Not surprisingly, the external auditor denies every one of CUMIS' ' accusations.

DEFENSE SUMMARY

Turner, Warren, Hwang and Conrad declares that in their lawsuit, CUMIS fails to provide evidence proving the external auditor committed professional negligence and that they breached the agreements entered into with Priority One Credit Union. What's more, they describe CUMIS' allegations as “uncertain, vague, and ambiguous” and add that as subrogee of the credit union, CUMIS does not possess the “legal capacity” in the state of California, to file a lawsuit against their firm. CUMIS is also accused of delaying filing of their lawsuit and in doing so, caused detriment to the auditing firm.

Turner, Warren, Hwang and Conrad further assert that Priority One Credit Union’s conduct created the opportunity which enabled the theft of more than $1 million from the Los Angeles branch and accuses the credit union of “Unclean hands”, a legal term which brings into question the ethical conduct of the infamous and scandal ridden credit union, its managing officers, and two governing bodies, i.e., the Board of Directors and Supervisory Committee.

Additionally, Turner, Warren, Hwang and Conrad states that the theft of more than $1 million was the result of acts committed by unnamed "others" and not their firm. So who are these "others" who allegedly committed acts including dispensing advice which created the opportunity for the theft of more than $1 million?

The persons, departments or governing bodies which may include:

- President Wiggington

- Former CFO, Saeid Raad

- Three COO's: Beatrice Walker (2010-2011); Cindy Garvin (2011-2012); and Yvonne Boutte (2012-Present)

- Vice President of Compliance, Patricia Loiacano

- Board Chair, Diedra Harris-Brooks, and the Board of Directors

- Supervisory Committee Chair, Cornelia Simmons, and the Supervisory Committee

- The Accounting Department

- The credit union's internal auditor

- Any other external consultants and/or auditors

DID SOMEONE SAY,

"PAST NEGLIGENCE"?

"PAST NEGLIGENCE"?

We recently came across the following 2007 article which we were previously unaware of. The article reminds us of the many security problems that have plagued Priority One since Charles R. Wiggington, Sr was appointed President. The lawsuits currently in litigation are the culmination of the President's inability to review the credit union's internal controls and introduce changes to resolve deficiencies found in Priority One's policies and procedures.

CONCLUSION

The Yellow M and M

Nowadays, Priority One' is best defined by its legal problems. The lawsuits filed each and every year since 2010 have exposed the unethical and abusive behaviors of President Charles R. Wiggington, Sr. and what seems to be his disdain for laws, policies and structure created to protect the credit union's assets. This same contempt towards rules is echoed by the Board of Directors and Supervisory Committee who have spent hundreds of thousands of dollars since 2007, ensuring President Wiggington remains in power.

The counter-complaint filed on June 4, 2015, by the credit union can reasonably be viewed as yet another attempt by Priority One's leadership to escape accountability for their failures to ensure security protocols were being practiced and to find a scapegoat who will be held culpable for the $1 million in cash from the Los Angeles branch.

With tremendous assistance by its insurance carrier, CUMIS, Priority One is now targeting its former external auditor, Turner, Warren, Hwang and Conrad and holding them responsible for the theft of more than $1 million in cash despite the fact CUMIS concluded that the credit union's security protocols were being maintained at the time the thefts occurred. So how did the credit union's allegedly well designed and effective security measures fail to identify or thwart the thefts that transpired during the years of 2010-2012?

The big question remains as to how a single employee, with or without assistance by an accomplice(s), could physically remove more than $1 million in cash from the Los Angeles branch's vault without detection by the Supervisory Committee, the Board of Directors, three COO's, the Vice President of Compliance, and President Wiggington?

The idea that several thefts occurred without detection brings into scrutiny the effectiveness of Priority One's policies and procedures designed to allegedly protect credit union and Member assets. We'd certainly like anyone from CUMIS to explain how they determined that Priority One's security implements are functioning at optimum.

As we've reported over the past six years, Priority One's executive sector and its Directors and Supervisors are gross incompetents, ignorant about the credit union's internal procedures that they allegedly are qualified to oversee. We hope Turner, Warren, Hwang, and Conrad's attorney will ask those important questions that will prove the competency or incompetency of the members of the credit union's two governing bodies.

When Charles R. Wiggington, Sr. was first appointed President, he was given a wonderful opportunity to lead the then growing credit union in a manner that befits a President of a Credit Union. Instead the inept officer chose to demonstrate his contempt towards laws and policies, ignoring what was beneficial to the Credit Union and seeking anything and everything needed to placate his bloated ego. Instead, the obstreperous and childish President chose to don all the dignity of the Yellow M and M and becoming the physical personification of everything that is counter-productive and or that is good for any business.

The counter-complaint filed on June 4, 2015, by the credit union can reasonably be viewed as yet another attempt by Priority One's leadership to escape accountability for their failures to ensure security protocols were being practiced and to find a scapegoat who will be held culpable for the $1 million in cash from the Los Angeles branch.

With tremendous assistance by its insurance carrier, CUMIS, Priority One is now targeting its former external auditor, Turner, Warren, Hwang and Conrad and holding them responsible for the theft of more than $1 million in cash despite the fact CUMIS concluded that the credit union's security protocols were being maintained at the time the thefts occurred. So how did the credit union's allegedly well designed and effective security measures fail to identify or thwart the thefts that transpired during the years of 2010-2012?

- Not only did the credit union's security protocols fail to deter the thefts of cash from the vault but in 2009, these same protocols failed to detect numerous internal thefts totaling more than $60,000 and perpetrated by a receptionist of the Los Angeles branch.

- And once again, these same protocols failed to stop a married couple of withdrawing more than $100,000 from a HELOC checking account whose term had expired.

The big question remains as to how a single employee, with or without assistance by an accomplice(s), could physically remove more than $1 million in cash from the Los Angeles branch's vault without detection by the Supervisory Committee, the Board of Directors, three COO's, the Vice President of Compliance, and President Wiggington?

The idea that several thefts occurred without detection brings into scrutiny the effectiveness of Priority One's policies and procedures designed to allegedly protect credit union and Member assets. We'd certainly like anyone from CUMIS to explain how they determined that Priority One's security implements are functioning at optimum.

As we've reported over the past six years, Priority One's executive sector and its Directors and Supervisors are gross incompetents, ignorant about the credit union's internal procedures that they allegedly are qualified to oversee. We hope Turner, Warren, Hwang, and Conrad's attorney will ask those important questions that will prove the competency or incompetency of the members of the credit union's two governing bodies.

When Charles R. Wiggington, Sr. was first appointed President, he was given a wonderful opportunity to lead the then growing credit union in a manner that befits a President of a Credit Union. Instead the inept officer chose to demonstrate his contempt towards laws and policies, ignoring what was beneficial to the Credit Union and seeking anything and everything needed to placate his bloated ego. Instead, the obstreperous and childish President chose to don all the dignity of the Yellow M and M and becoming the physical personification of everything that is counter-productive and or that is good for any business.